Renters may sometimes feel that they’re “throwing away money” to their landlord with each monthly payment. After all, a homeowner gets to build equity in their property with the monthly home loan payment. But does this mean that owning a home is better than renting? Well, the answer may not definitely be a ‘Yes’.

While buying a home can have financial benefits in the long term, it also comes with many additional costs that can make it more expensive than renting in the short term.

Here are five factors to consider as you decide on your options.

-

Your financial position

When considering to buy or rent, you must first establish whether you can afford it or not.

One way to find out whether you are ready to purchase is by calculating your Debt Service Ratio (DSR). This is a ratio that calculates an individual’s debt to their income.

DSR Formula = Debt/Net Income x 100

Banks will check whether your DSR is good enough for you to be able to pay your monthly instalments until your loan is completed. A DSR more than 70% is generally not accepted by banks.

There are many hidden costs in home ownership. Besides the 10% down payment, there are also other costs such as legal fees, stamp duty charges and processing fees that you need to prepare before purchasing. Make sure that you can also continue to pay the monthly loan instalments without fail.

-

The price-to-rent ratio

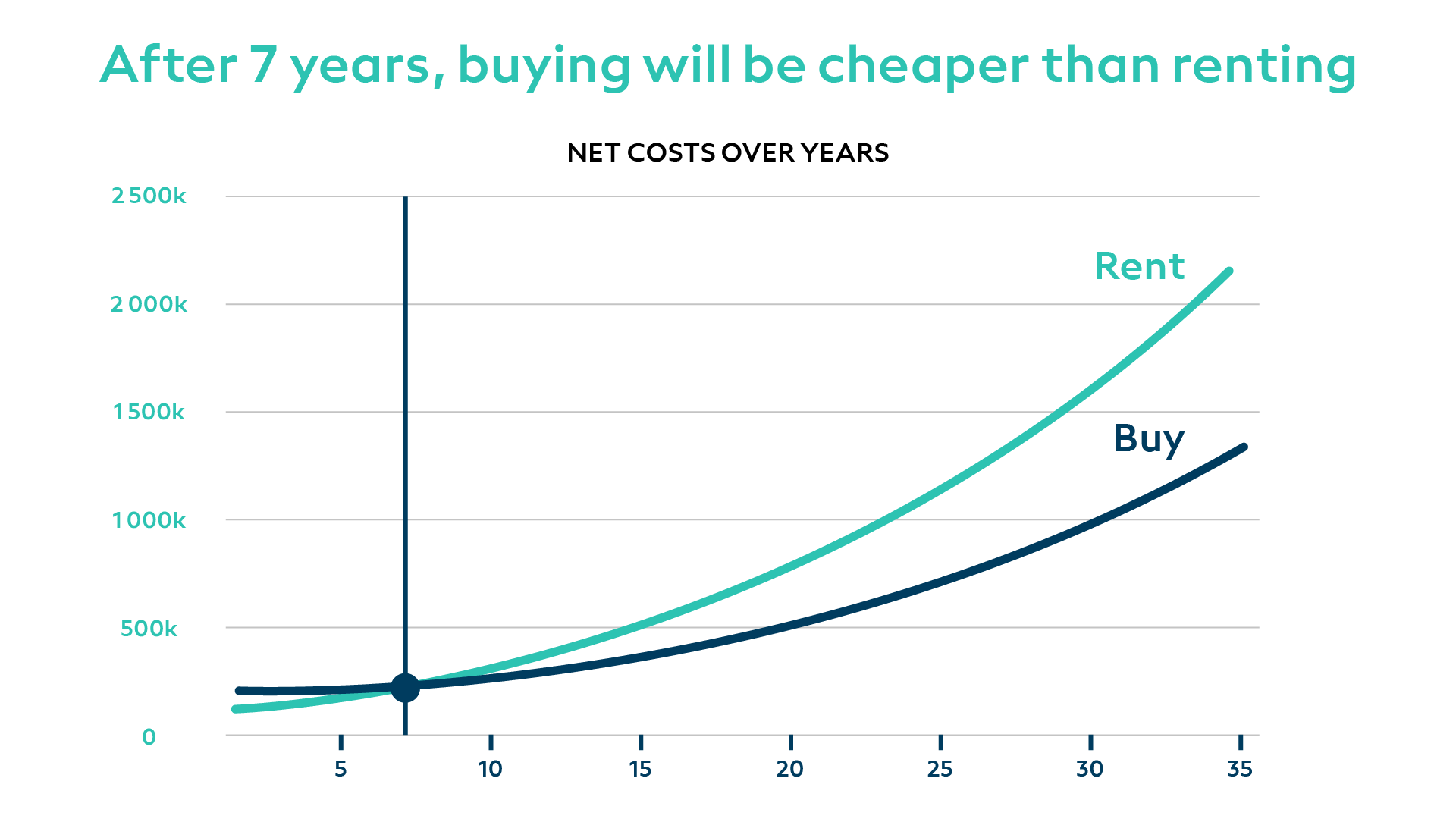

To know if buying or renting a property is the better option, you can calculate the price-to-rent ratio of that property. Price-to-rent ratio indicates the number of years your rental fees will take to match the cost price of a property. This ratio is calculated by dividing the annual rental sum from the average cost of the property.

For example, if we compare renting to purchasing a property that costs RM500,000, below are a few assumptions:

Renting

- Rent: RM1,500 a month, increases by 3% every year on average

- Money that is saved from not buying the home is invested, with a return of 7% a year

Buying

- Price of home: RM500,000, appreciates by 4% every year

- Down payment: 10%, which is RM50,000

- Monthly instalment: RM2,280.08 (4.5% interest rate, 35-year tenure)

- Upfront costs of buying (legal fees, stamp duty, etc): RM25,000

- Maintenance costs: RM200 a month

Source: imoney.my

The calculation above shows that renting is cheaper than buying, but only for the first six years. After that, buying becomes cheaper.

-

The duration of your stay

Are you looking for a temporary accommodation or do you want to settle down for at least the next 10 years?

It only makes sense that purchasing is not worth it if you’re planning on staying at the property for a short while.

However, if you are looking to establish long-term living with the possibility of all your future plans taking place within a property, then plan your finances to purchase the property accordingly.

-

Your needs and preferences

When it comes to deciding on buying or renting, another factor is your lifestyle needs and preferences.

For example, if you are not too keen on purchasing a property in the outskirts, but your workplace is located in a sub-urban area, renting a property nearby will be much more sensible than buying.

On the other hand, buying a property gives you full rights to renovate or decorate it according to your whims and fancies. If you’re the type of person who loves experimenting with renovations and decorations, buying would be a better option, because with renting, you might be restricted by the conditions on your tenancy agreement.

-

Can you bear the cost of being a homeowner?

Do remember that if you are buying a property, as a homeowner, you also have to service a few expenses other than the monthly loan instalment.

These include:

- Quit rent or cukai tanah for landed properties

- Property assessment or cukai pintu tax

- Maintenance fees and sinking fund

When renting, any repair within the property that is considered major works will usually be done by the owner.

So, Which Is Right For Me?

There are many pros and cons for both renting and buying, and what’s right for an individual depends on their own unique situation. Just because renting is cheaper in the short term doesn’t mean you shouldn’t consider buying a home, but getting tied down with a home loan when you’re not financially stable isn’t the right move either. You have to consider your financial situation and goals, the cost of renting and buying in the local property market, and the terms of a home loan you can qualify for.

The strength of your current credit score will also allow you to obtain more favourable loan rates and terms that can save you money.

The statement and information in the articles are the opinion of the writer and meant only as a guide. Any property purchase, rental or lease involve many legal issues and other complication depending on the individual facts and circumstances. Readers and Users are strongly advised to seek professional advise including from qualified and competent lawyers, bankers and/or real estate agent to verify the information and the statement before embarking on any purchase, rent or lease of any property. To the fullest extent permitted by law, we exclude and disclaim liability for any losses and damages of whatever nature and howsoever cause and arising including without limitation, any direct, indirect, general, special, punitive, incidental or consequential.